The financial world in 2026 has seen a major shift in how younger generations handle their cash. Millennials now prefer to use High-Yield Savings Accounts which provide stable returns instead of the “get rich quick” crypto and meme stock era which dominated early 2020s.

The Return of “Real” Interest Rates

For almost ten years savings accounts provided an insulting 0.01% interest rate. The top HYSAs in 2026 provide interest rates between 3.5% and 4.2% APY despite a slight decrease from the 2024 peak. The “cost” of keeping funds in a regular big-bank checking account has become too high for people to overlook.

Protection Against Persistent Inflation

Millennials have experienced a loss of purchasing power because of inflation during the past few years. People now view high-yield accounts as both protective instruments and their original purpose for saving funds. The emergency fund allows them to accumulate sufficient funds to cover increasing grocery and rent expenses.

The “Safety First” Mindset Post-Market Volatility

After experiencing major stock market fluctuations and the failure of various “alternative” investments, Millennials now seek secure investment options. A HYSA offers people psychological protection through its FDIC insurance which covers up to $250,000 because it provides security that high-risk assets cannot deliver.

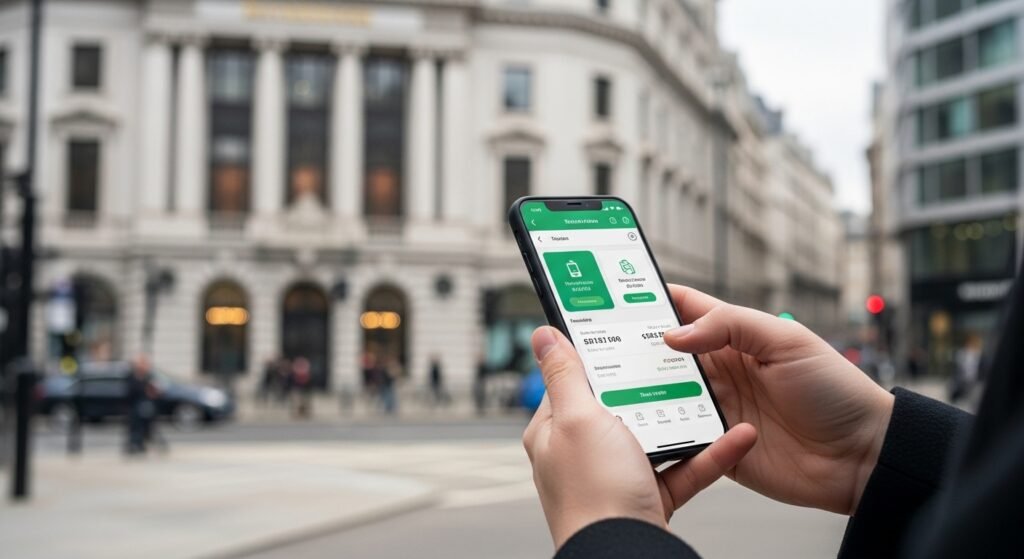

Digital-First Banking Habits

Online-only banks became the first fully accepted banking method for Millennials who represented the initial generation to use such services. Banks without physical locations decrease operational costs which enables them to deliver better customer service through higher interest rates. The HYSAs have become the standard option for 2026 because people can effortlessly create accounts through their smartphones within five minutes.

The “Loud Budgeting” Trend

Social media trends like “Loud Budgeting”—where people are vocal about saving money rather than spending it—have made financial literacy “cool.” The movement implements high-yield accounts as its main instrument because they allow customers to track their monthly savings through visible interest payments.

Automation and “Set-and-Forget” Saving

Advanced automation capabilities come with modern HYSAs. Millennials separate their income through “buckets” or “vaults” which let them automatically allocate funds towards various objectives including home purchases and wedding expenses. People can stop making choices about their finances because this method ensures they will save money first before any spending occurs.

Liquidity in an Uncertain Job Market

A HYSA provides “liquid” money access which differs from both 401(k) accounts and Certificate of Deposit (CD) products. Millennials need instant cash access because AI-driven corporate restructuring makes job loss possible at any moment.

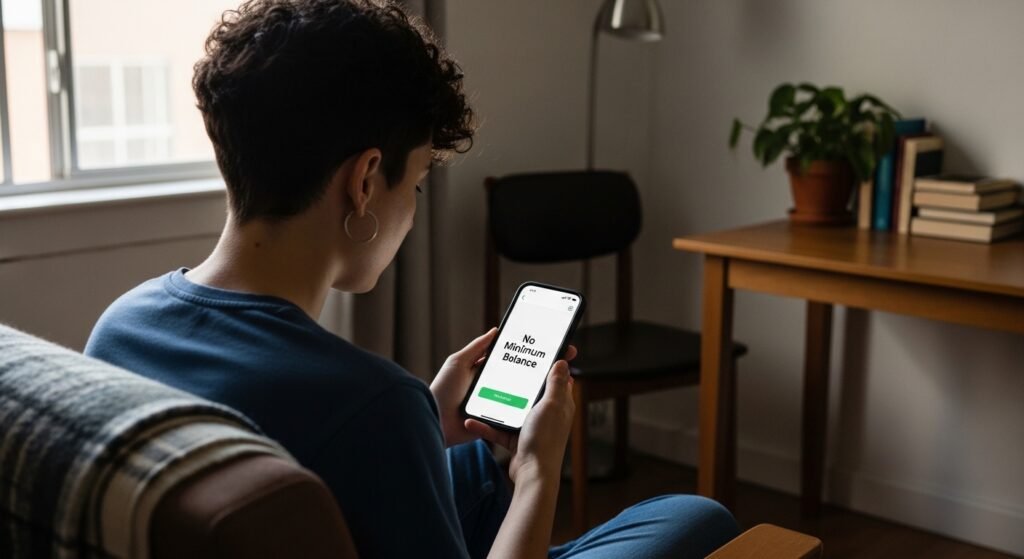

Lower Barriers to Entry

The previous requirements for opening high-interest accounts mandated customers to maintain a balance of at least $10,000. Most top-tier online HYSAs in 2026 require no minimum balance and charge no monthly fees. Younger Millennials who just began their professional journey can now access high-interest banking services thanks to this banking system.

The “Side Hustle” Tax Buffer

Millennials who work in the creator economy and freelance industry use HYSAs to save their tax obligations. They keep their tax money in a high-yield account for one year to earn interest on funds which they do not actually own.

The Death of the Traditional “Big Bank” Loyalty

Banks called the “Big Four” have lost their brand loyalty among Millennials. People tend to move their money based on which bank provides them better interest rates because they want higher financial gains. The banks need to maintain high-interest rates because their clients will leave for competing banks which offer better deals than their current bank.