The total amount of credit card debt held by Americans has climbed to an all-time high, surpassing previous peaks by a significant margin. While having a balance isn’t always a crisis the combination of record debt levels and high interest rates has created a perfect storm for many households. The real danger resides beyond the statement’s number because that number creates permanent constraints on your ability to achieve financial independence.

The Trap of Compound Interest

Credit card interest creates daily compounding interest charges which differ from car loans and mortgages that use different compounding methods. This means you are paying interest on your interest. When debt reaches record levels the cycle becomes more intense because it creates an impression that the debt balance continues to rise without any new purchases.

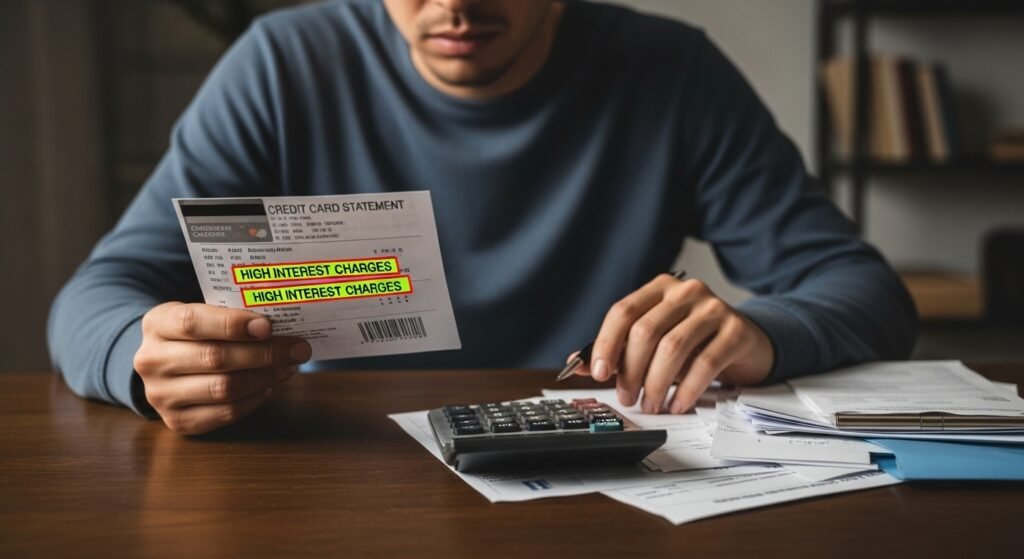

Interest Rates are at Historic Highs

The average credit card interest rate has reached a level that exceeds 20 percent. The cost of borrowing at this point has reached an extraordinary level. Even a small balance grows into a large amount because most of the monthly payment goes toward interest instead of paying off the principal amount.

The Minimum Payment Mirage

The balance will require decades to pay off if you pay only the minimum amount required. Credit card companies design minimum payments to keep you in debt for as long as possible. The minimum payment requirement on a record-high balance only allows you to pay off the interest amount.

It Siphons Your Monthly Cash Flow

Every dollar that goes toward paying off old debt is a dollar that cannot be used for current needs. High debt levels act like a hidden tax on your income which reduces your available funds for groceries rent and emergency savings.

Impact on Your Credit Score

One of the biggest factors in your credit score is credit utilization—how much of your available limit you are using. High balances can crush your score which makes it difficult to obtain a mortgage or car loan because it becomes more expensive or completely blocked.

The Risk of Floating Expenses

Many people use credit cards to cover basic necessities when their paycheck falls short. The danger is that this creates a reliance on debt for survival. The household loses all essential purchasing power when it reaches its credit limit.

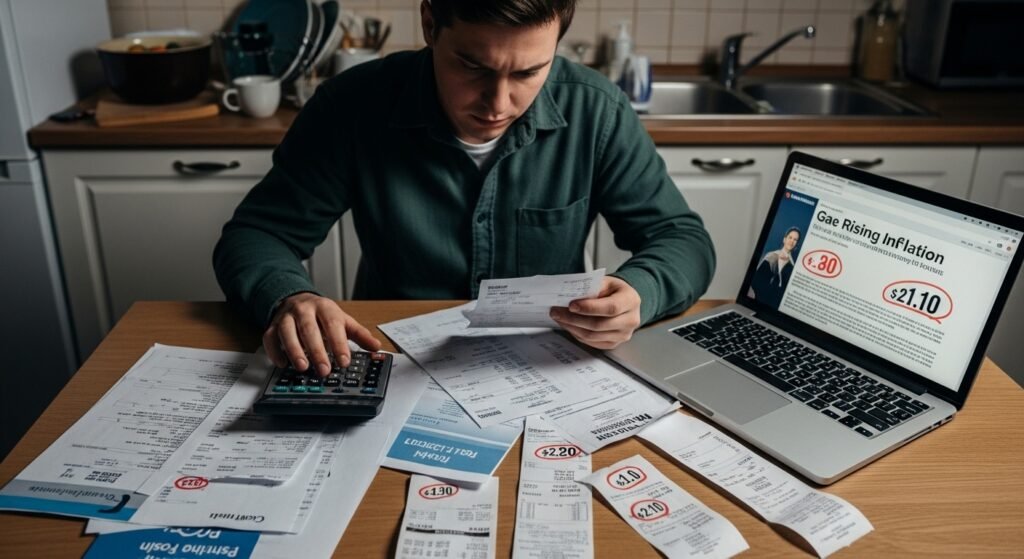

Inflation’s Double-Edged Sword

People use credit cards more when living expenses rise because they need to maintain their current spending levels. High debt levels increase your risk of inflated prices. You have to purchase the earlier more expensive items with the current dollar value.

Reduced Financial Resilience

The real danger of high debt exists because it eliminates all protection against financial emergencies. You will end up bankrupting your resources because you lack credit card space to cover essential needs after losing your job or facing a medical emergency.

The Psychological Burden

Carrying record-breaking debt causes chronic stress anxiety and even physical health problems. The mental load creates performance problems at work and home which exhausts you and leads to financial paralysis.