U.S. personal finance professionals like Dave Ramsey consider Zero-Based Budgeting to be the best method for people to manage their finances because it enables them to gain complete financial control. The fundamental principle states that all your earnings should match your expenditures to reach a balance of zero. Your bank account balance does not reach zero at month-end; instead, you have designated every dollar you earned to fulfill a specific purpose.

Give Every Dollar a “Job”

Zero-based budgeting requires you to dedicate every dollar in your bank account to a specific function because it prohibits any unallocated funds from existing in your account. Every penny you own must receive precise instructions about its destination before the month begins including all expenses from rent to groceries to movie tickets.

Start with Your Total Income

List everything money that you expect to receive this month. All your income sources should include your main after-tax paycheck plus your side job income and tax refunds and any five-dollar gifts from your grandmother. The first step of your process involves identifying all your available financial resources.

Focus on the “Four Walls” First

The American budgeting system requires you to first allocate your financial resources toward covering your basic needs which include food and utility services and housing and transportation expenses. These basic requirements exist to protect your physical safety and enable you to maintain your work productivity. All other expenses must be handled after these essential needs have been satisfied.

Justify Every Expense

Zero-based budgeting requires you to begin at zero because it demands complete justification for all expenses rather than allowing you to duplicate previous month spending. You must evaluate all your expenses from streaming services to gym membership costs to determine their actual value for the current month.

Account for “Sinking Funds”

Americans establish sinking funds to handle their major expenses which occur at irregular intervals throughout the year including Christmas shopping and car insurance payments and annual veterinary checkups. You build a financial reserve by saving a fixed monthly amount which will ensure you have cash available when the large expense comes due.

Prioritize Debt Repayment

Zero-based budgeting becomes an effective tool for managing your finances when you have credit card debt or student loans to repay. The budget will help you see your available surplus funds which should then be used to pay off your smallest debt first in order to create repayment momentum.

Don’t Forget “Miscellaneous”

The unpredictable nature of life requires you to maintain a small category that functions as an emergency fund for unexpected expenses. You need to establish a minor”oops” fund which covers all unplanned costs that arise from missing a birthday present or dealing with a flat tire. A budget allocation for unexpected expenses will stop you from exceeding your budget limits when unplanned events happen.

Use the “Envelope System”

Many people who use zero-based budgeting choose to work with physical envelopes or digital envelopes to manage their budget. You budget for groceries by putting the total amount of $400 into an envelope. You must stop spending money in that category after you have used up all the funds for the month.

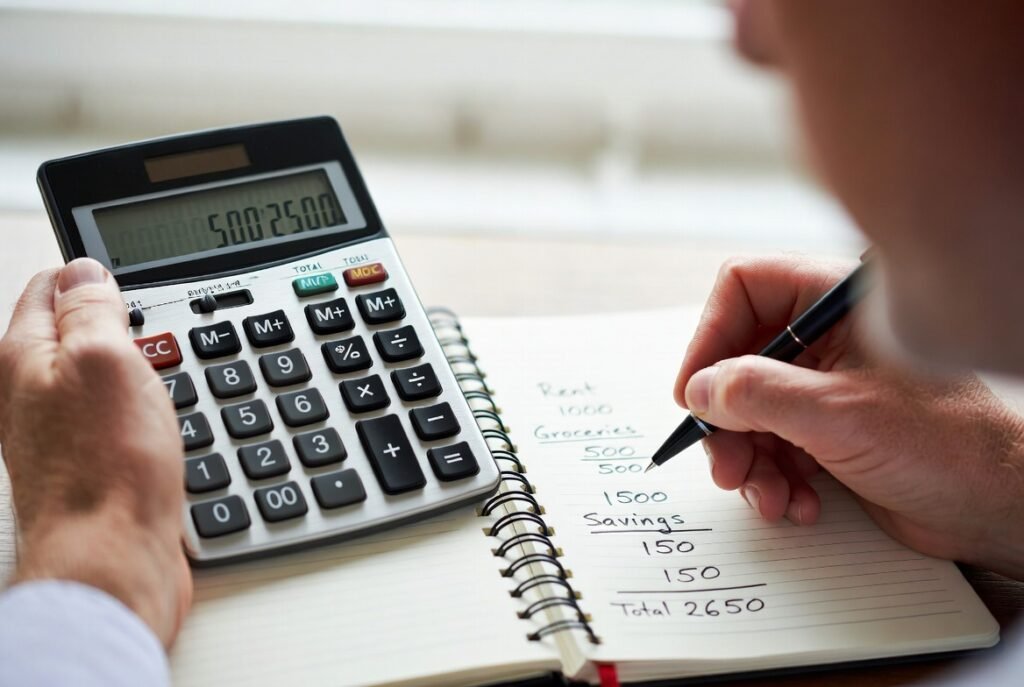

Subtract Until You Reach Zero

This is the “math” part. You need to deduct all your expenses which include savings and debts and entertainment costs and bills until you reach exactly zero. You should allocate any remaining balance of $50 between savings and debt repayment.

Track Your Progress Daily

Tracking the budget functions as the movement that follows the budget plan creation. You need to document all your daily expenses because it helps you control your spending limits for each category. Americans prefer to use mobile apps like EveryDollar and YNAB for tracking their expenses while they are out.