Early retirement requires more than a substantial income because it demands people to control their finances while changing their spending habits toward asset creation. You can regain lost years from the office by establishing strategic habits which support your long-term goals and help you avoid immediate rewards. The expert-backed financial independence strategies which follow can be achieved through discipline and discipline and smart financial management.

Maximize Your Savings Rate

Your ability to save money from your income functions as the primary requirement for achieving early retirement. Standard advice recommends a 10% saving rate but experts who study early retirement recommend professional saving rates between 30% and 50% of their income. Your financial situation enables you to build wealth through extreme frugality which produces excess funds that you should invest in assets that generate income to minimize your work time.

Prioritize Compound Interest

Your ability to create wealth depends on your best friend – time. Your money starts to make additional money through early and regular investing which creates a compounding effect. The market handles your capital growth better when your investment stays in the market for an extended period because it generates more returns than your initial investment.

Eliminate High-Interest Debt

Your ability to create wealth suffers when you pay credit card companies interest rates that exceed double digits. Experts endorse aggressive debt repayment as the most effective method to achieve guaranteed investment returns. Your monthly cash flow will increase when you eliminate debt because the debt payments you previously made will be redirected toward your retirement savings.

Master the 4% Rule

This simple guideline helps you determine your “retirement number.” The withdrawal rate of 4percent per year from your complete investment portfolio should provide you with three decades of financial support according to this rule and your financial independence goal requires you to multiply your yearly spending estimate by 25 and reach that total amount.

Adopt a Minimalist Lifestyle

The most effective retirement strategy requires you to decrease your monthly expenses. Your expense requirements decrease when you evaluate every purchase decision while prioritizing experiential activities above material possessions. Your current savings increase while your retirement expenses decrease because of this.

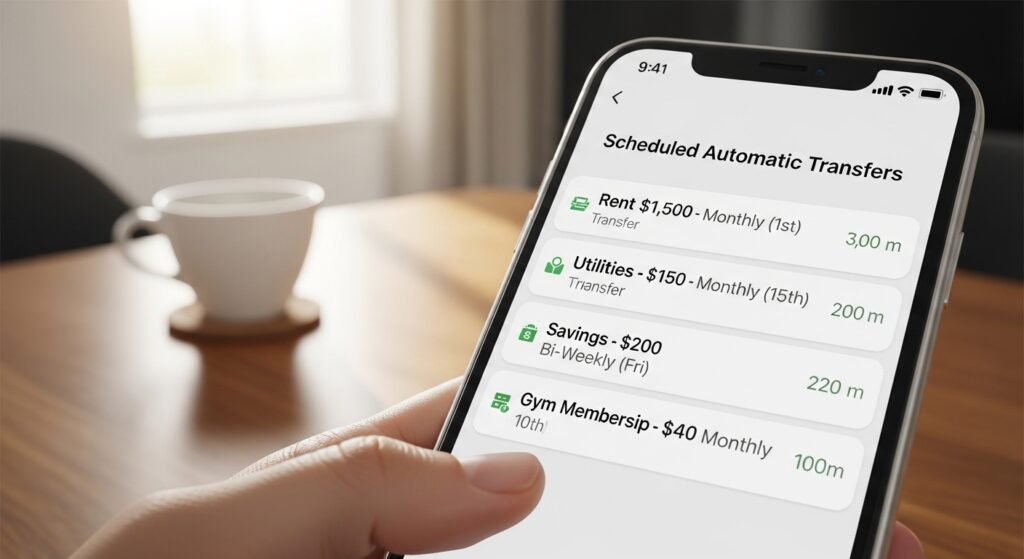

Automate Your Finances

Decision fatigue can lead to poor spending choices. Experts recommend that you should establish automatic payment systems which transfer money to your savings and investment accounts immediately after you receive your paycheck. You will automatically decrease your spending when your budget gets depleted before you can see the actual amount that remains.

Utilize Tax-Advantaged Accounts

Employer-sponsored plans and individual retirement accounts provide access to government funds which act as free money according to those who use them. These accounts enable taxpayers to either decrease their present taxable income or experience tax-free investment growth which helps them retain more of their earnings instead of paying taxes.

Create Multiple Income Streams

A 9-to-5 job acts as a lengthy process which delays your ability to achieve financial independence. Your side hustles and dividend-paying portfolios and rental income will act as a financial safety net which helps you achieve your saving goals more quickly. Multiple income streams enable people to balance their financial interests with their market risks because they help build wealth faster.

Focus on Low-Cost Index Funds

Many experts recommend investors to choose broad-market index funds rather than selecting individual stocks according to their findings. These funds enable instant distribution of their investment across hundreds of companies through their lower fee structure. The lower management fees of this investment option will lead to savings which exceed hundreds of thousands of dollars because it prevents loss to Wall Street.

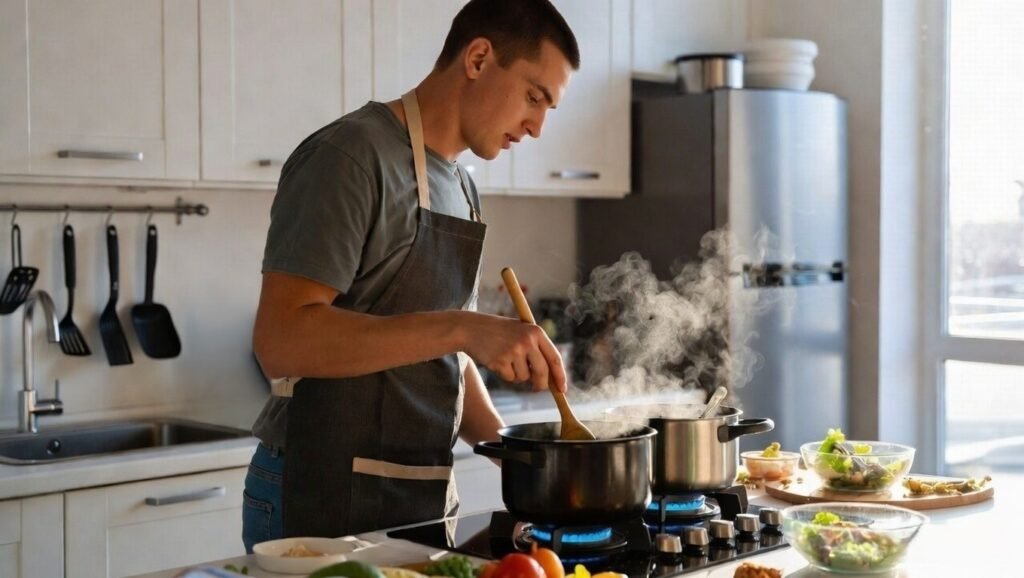

Cook at Home Frequently

The modern budget experiences its most substantial financial loss through expenses related to dining out and food delivery services. The process of saving for groceries and preparing meals generates significant financial benefits which continue to accumulate over the course of ten years. Your income will increase significantly when you perceive food as a source of energy instead of a main entertainment option.