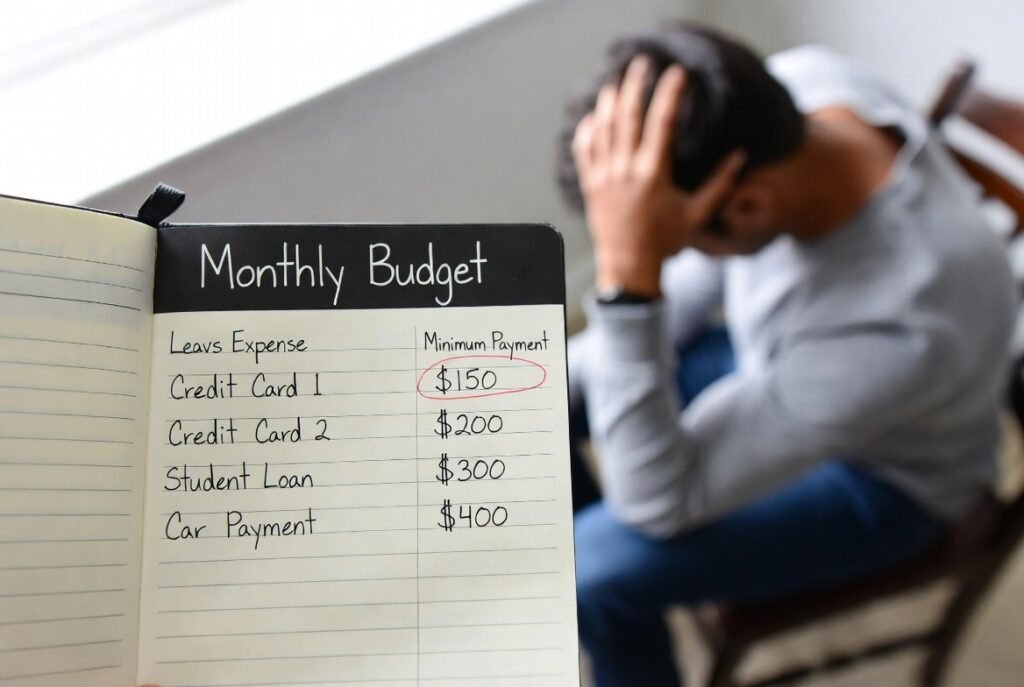

The balances in credit cards are also recording some changes as the economic conditions and consumers change. The increasing cost of living, interest rate variations, and shifting purchasing patterns are all affecting the usage of credit cards in people’s hands. These developments provide valuable indications on domestic finances and the overall economic well-being.

Greater Average Balances per Month

The mean balance held on credit cards per month has gone up. Consumers are also settling smaller balances than they did in the past. This shows that there is a change from short-term borrowing to long-term borrowing.

Rising Interest Charges

The rates on credit card balances are becoming higher and entailing interests. Increased interest increases the cost of carrying balances. There are numerous consumers who are incurring high interest payments despite the same spending. This trend brings into focus the increase in the cost of borrowing.

Slower Balance Paydowns

Consumers are also taking their time to pay off their credit card debt. Minimal payments are on the increase, and full balance payments are on the decrease. The behavior is an indicator of financial distress and low savings. Reduced paydowns may result in an increase in debt levels.

Growth in Revolving Debt

Rollover credit card debt is still increasing because consumers are taking balances on a monthly basis. It implies that it is dependent on credit as a financial instrument, but not on convenience. Although revolving debt is flexible, it is also very expensive in terms of interest rates.

Increased rates of use of credit

The use of credit is growing with the expansion of balances in comparison to credit limits. The increased usage may affect the credit scores negatively. This tendency indicates that buyers are spending more of the credit they have.

More Balance Transfers

The balance transfer business is on the rise because consumers want lower interest rates. Others are transferring debts to cards with promotional offers in order to save on the interest expenses. This is an indication that they are conscious of the increasing borrowing costs.

Increased Minimum Payments

Minimum payment is becoming a popular form of repayment. This maintains accounts up to date but retards debt reduction. Minimisation of payment depends on the minimum payments that add to the interest paid in the long run. This trend implies short-run cash flow strains.

Drift to Digital Expenditure

Online and digital purchases are also increasing credit card balances. The simplicity of payment stimulates a high frequency of transactions with small amounts, which accumulate rapidly. The change has an impact on spending awareness and budgeting.

Rising Delinquency Rates

There is an indication of growth in delinquency rates on credit cards. Certain consumers are found to be finding it hard to make payments. The trend is associated with financial pressure and increased debt obligations.

Consumer Spending Behavior Changes

Economic uncertainty is forcing consumers to change their spending patterns. There may be a reduction in discretionary spending and an increase in essential spending. The income gaps are normally bridged by the use of credit cards. The transition speaks of shifting priorities and conservative financial habits.

Heightened attention to Credit Limit

There are lenders who set credit limits according to the risk assessment. The limit might decrease or stay constant when consumers witness an increase in the balance. The change is capable of limiting access to more credit. It is a warning by lenders because of the increase in debt.

Increasing Sensitivity to Debt Management

There is an increase in the number of consumers recognising the importance of using credit cards wisely. There is more interest in educational materials and financial instruments. This concern is an indication of fear of increasing balances and interest payments.